Analytics For Employers: A Tutorial (Part 2)

Healthcare

A succinct guide on how to use analytics to save money on healthcare.

Over the past 3 years, the most common question we have heard from employers and brokers is this: health analytics is good, but what do we do with the data? Well, we are going to answer that question in this very post. That’s right, we’re sharing all the most actionable areas we look at for self-insured employers to help them to gain control over their spending. Some may say that we’re giving away our secrets, but we don’t see it that way. Our mission for employers is to make them savvy health care consumers, so making information transparent is what we do. Furthermore, it’s important to open up conversations on how organizations are using analytic data, because these conversations will help to advance insight and foresight so employers can use their data to create, track and refine a long-term strategy for the benefits they offer.

In Part 1 of this post we established that for employers, the best strategy for using health analytics moves beyond simply looking at spending to enter the realm of strategic benefit planning. This is the limitation of traditional healthcare analytics. Over the next decade, we will continue to see employers move away from watching spending go up and down and move towards looking at data in a way that provides both insight and foresight into population health. The next evolution of employer analytics informs a deeper understanding of who associates are, the benefits that will attract the best talent, and identifying the optimal strategy for funding these next-generation benefits packages.

To start, we pulled together a list of areas that any employer can explore if they want to ensure they’re using data to guide their spending decisions on health benefits. We’ve broken this into 3 sections: 1) Goals, 2) What’s Actionable? and 3) Areas of Insight.

Beginning with the end in mind, here are the top goals that self-insured employers have when it comes to monitoring their health spending:

Goals:

1. To cut excess and wasteful healthcare spending and to accurately project future spending. Approximately 20% of an employer’s healthcare spending is wasted due to unnecessary and preventable costs. Open access to data helps to inform employers on exactly what areas are driving wasteful spending and how to better predict future spending.

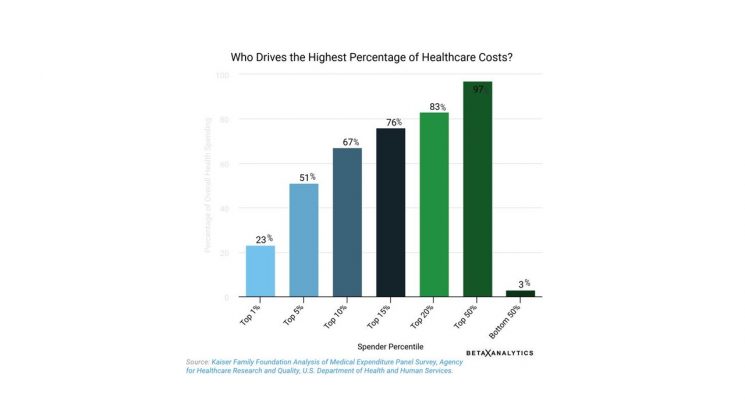

2. Identify strategies to support associates on their health journeys. While 5% of people drive 51% of health costs, 50% of plan members account for only 3% of health spending. Understanding how to support the unique, complex health needs of members affects a company’s bottom line in both healthcare costs and employee productivity.

3. Track progress on the current healthcare and wellbeing strategy. An unbiased evaluation of a healthcare program is eye-opening. Not only does it guide the strategic evolution of an employer’s healthcare strategy, it may reveal opportunities to recoup hefty vendor performance guarantees.

4. Make sure members are getting the preventative medical attention they need. We consistently see that between 10%-20% of members never see a doctor. It’s within this group of people who are notdriving costs today where an employer’s greatest future healthcare risks can lie.

In order to meet these goals, an organization needs to identify what exactly can be actionable. It’s easy to spot the costs that stick out, but when is it too late to intervene on a cost-driver? Here are the most common areas where employers can focus to influence spending, care quality, preventative care, and effectiveness of condition management.

What Is Actionable?

· The plan’s pharmacy formulary (with some limitations based on the PBM partner).

· The plan’s rules surrounding specialty medications.

· The healthcare partners the employer selects (health plan, PBM, condition management services, smoking cessation, behavioral health services, direct primary care, centers of excellence).

· Plan contributions, deductibles and coinsurance paid by employees for their healthcare benefit, emergency room surcharges, spousal surcharges, smoker surcharges, stop loss arrangements.

· Cost variation among high cost and/or high volume services (MRIs, musculoskeletal surgeries, cancer care, etc).

· Effectiveness of member education on health benefits.

· Targeted wellbeing services offered to members.

Now that we’ve laid out the goals of using data and the areas that are actionable, here are some specific questions to answer when looking at the data.

Areas of insight.

1. Which conditions and medications represent the largest population health risks? How do these conditions vary by both dollars spent and number of people affected?

2. Can amending prescription drug policies surrounding step therapy, specialty drugs, generics, place of service/purchase lead to savings for members?

3. Does the member base have a problem with emergency room (ER) misuse and are certain locations or member categories driving ER costs?

4. Do changes in member risk score, medication adherence and prevalent disease states such as diabetes show that your investments in condition management, smoking cessation and wellbeing interventions are working? Could performance guarantee fees be recovered from vendors?

5. Are there trends noticeable related to members who are not engaging with physicians at all? Through looking at healthcare utilization among work location, salary bands, plan types—can we identify trends as to why certain people are not using necessary health services? These barriers to accessing care could be cost, lack of understanding of benefits, and even corporate culture, among others.

6. What percentage of people are receiving preventative care and age-appropriate screenings among various member demographics?

7. What are the largest cost variances that can be actionable? For example, could costs associated with procedures such as joint and hip replacement surgery or even MRIs be standardized via options that are available to your members? (Could centers of excellence be leveraged?)

8. Could a direct primary care model have benefit for the member population?

9. Are there actionable insights with respect to absence data and workers compensation claims?

10. What is the size and scope (in dollars and members) of opioid use and dependency-related costs?

In the same way that reading an abstract is not the same as reading the book, please keep in mind that this is a very brief overview of a complex subject.* Every employer has unique challenges related to population health and health spending, so there’s is no real “one size fits all” approach. The data drives the discussion in a unique direction for each employer.

* * *

About BetaXAnalytics:

We combine data science with clinical, pharmacy and wellness expertise to guide employers and providers into a data deep-dive that is more comprehensive than any data platform on the market today. BetaXAnalytics uses the power of their health data “for good” to improve the cost and quality of health care. For more insights on using data to drive healthcare, pharmacy and wellbeing decisions, follow BetaXAnalytics on Twitter @betaxanalytics, Facebook @bxanalytics and LinkedIn at BetaXAnalytics.

* A Note on Data Privacy The purpose of using health analytics is to identify actionable areas to target costs and to improve effectiveness of care options on an aggregate level. This is done by looking at trends in data and under no circumstances should insights be presented to an employer in a way where data is individually identifiable. There are a number of data-related best practices that we recommend to remain adherent to privacy laws. Any employer, broker or consultant who is using health analytics should do so under strict adherence to HIPAA regulations and under the advisement of an experienced data privacy attorney.